Good morning.

If you thought your firm’s tech budget was already high, have a seat.

Wealth management companies are expected to more than double their AI spends over the next three to five years, according to a survey from consulting company Wipro. Right now, less than half use AI extensively, but the majority of those managers say they have experienced significant competitive advantages.

Advisors also expect the tech will help build stronger relationships with clients. Who would’ve thought AI would actually bring us closer together?

Do Elections Matter to Markets?

Will the presidential election impact the markets? It all depends on who you ask.

For BlackRock founder and CEO Larry Fink, the answer is a resounding no. The leader of the world’s largest asset manager told a SIFMA conference last week that he’s simply tired of hearing that November’s election will have any lasting consequences. “The reality is, over time, it doesn’t matter,” he said.

Still, that hasn’t stopped advisors and portfolio managers from shifting a few things around. The majority of some 400 institutional investors surveyed by Prudential agreed that elections influenced portfolio allocation. “Markets tend to get a bit jumpy around election time,” said Aaron Cirksena, founder of the advisory firm MDRN Capital. “That’s usually short-lived.”

Fund Raising?

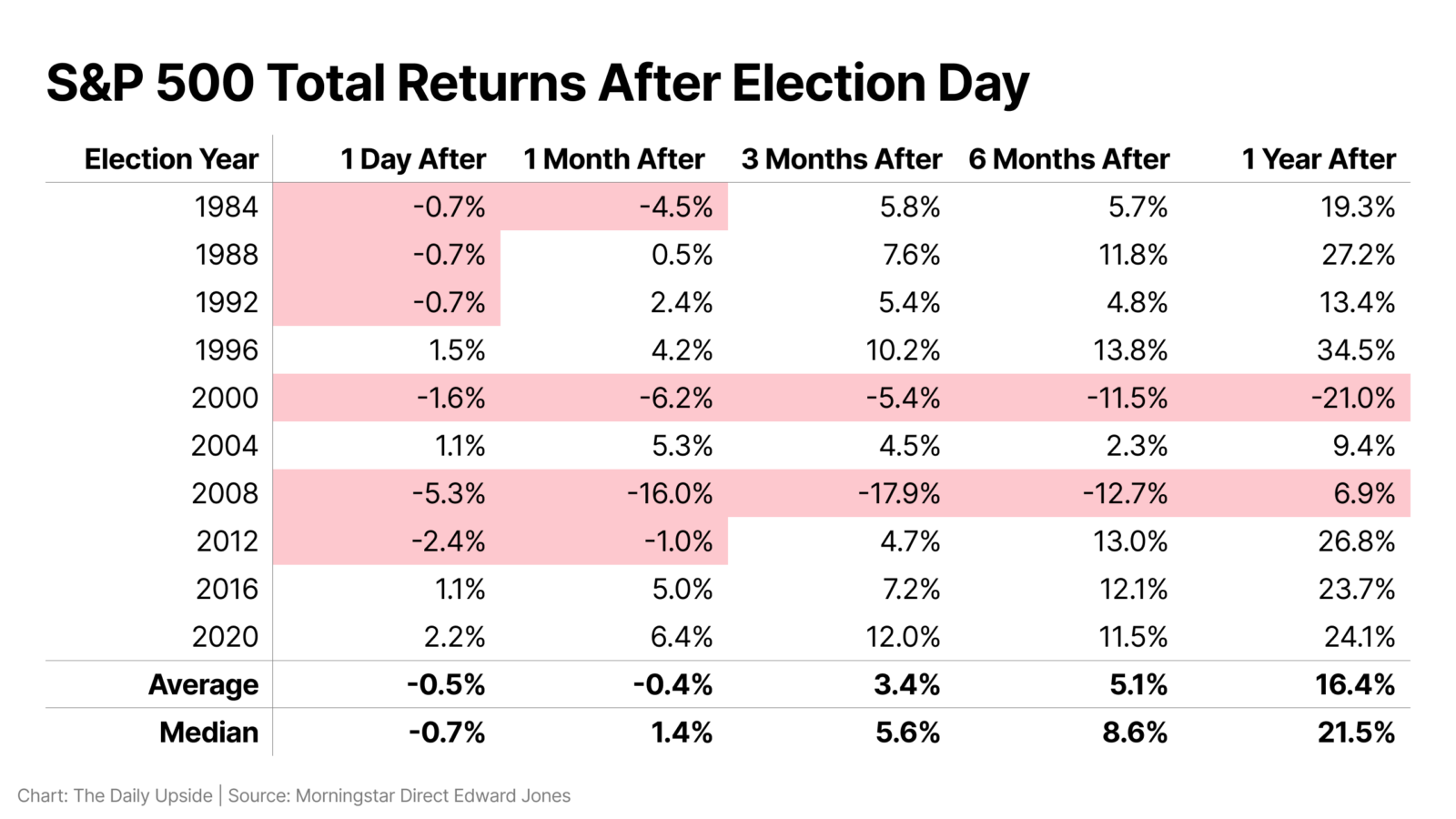

Stock market returns under both President Joe Biden and former President Donald Trump have been almost identical during their administrations. The S&P 500 returned 14% per year after dividends under each president, according to Edward Jones’ data. Going back a bit further, the index’s average annualized price return, not including dividends, was 9.6% when a Democrat won and 5.7% when a Republican won over the past 23 election cycles.

While the markets may not care who’s in the Oval Office, investors are bracing their portfolios for fallout come November anyway. More than half of investors globally said that elections are a factor in their decision-making, while just 1 in 5 said they didn’t matter at all, according to the Prudential study. The survey also found:

- 38% of US investors expect 2024 elections and their repercussions to influence portfolio changes.

- Roughly 4 in 10 investors said they have moved into cash to manage risk.

- Top concerns ahead of election day: the national debt, economic growth, and immigration.

Rock the Vote. Election time can be good for fine-tuning, but not big moves, Cirksena said. Historically, economic fundamentals will almost always pull the market back into balance within months post-election. Advisors may want to make minor adjustments, but overhauling portfolios just for an election rarely makes sense.

Strategies like dollar-cost averaging can help smooth out any wild swings and keep clients on track. For tax strategies, adjustments can help take advantage of the current tax landscape rather than bracing for major shifts, he said.

Keep in mind, market crashes and economic crises have happened during both Democratic and Republican administrations with every president — except George H.W. Bush — being in the White House during a bear market. Basically, free market capitalism just doesn’t care about politics. “Election-related shifts are often more noise than long-term disruption,” Cirksena told The Daily Upside.

Secrets To A Thriving Firm: Fostering Next-Gen Talent

Every winning team has its veterans and all-stars, but an oft-overlooked aspect of building an enduring franchise is recruiting and nurturing up-and-coming talent.

Sports analogies aside 一 the firms that take concrete steps to set up younger advisors for success are simply better positioned for sustainable growth.

And almost on cue, Commonwealth’s Practice Management team just released a Q&A highlighting the 4-step process to becoming a master mentor to young advisors. Learn how to:

- Locate ideal candidates for your firm

- Accelerate professional development

- Leverage tech to grow your client base

Dial in your coaching approach to get the most out of your advisors, contributing to both their professional growth and your firm’s bottom line.

How Advisors Can Help Turn 529s Into Roth IRAs

Advisors always tell clients looking to save for retirement to “start while you’re young.” Now, there’s an easier way to do that.

This year, under the SECURE 2.0 Act, unused savings from 529 plans — designed for college, K-12, and apprenticeship programs — can transfer to a Roth IRA tax-free, up to a certain point. Roughly 4 in 10 students graduate from a four-year public college without any debt, and 35% of parents say their children might skip college entirely, so rollovers can significantly benefit younger generations as they start saving for retirement.

“It’s understandable that [parents] might be wary about the tax implications of needing to withdraw those funds if they’re not used for education,” said Tony Durkan, head of 529 relationship management at Fidelity Investments. “These new legislative changes remove some of that worry while also providing the opportunity to give beneficiaries a leg-up on their retirement savings.”

Sit, Stay, Roll Over

Beneficiaries of 529 plans might have remaining funds due to lower tuition costs, scholarships, or not attending college. However, the SECURE 2.0 Act has a few stipulations for that money to roll over into a Roth IRA:

- Rollovers will only be eligible from 529 plans that have been open for at least 15 years, and they can’t come from contributions added in the last five years.

- The tax-free rollover limit tops out at $35,000, and the Roth IRA has to be tied to the beneficiary of the 529 plan.

The Internal Revenue Service still needs to clarify some details, especially regarding whether the 15-year rule resets if the 529 beneficiary changes. “Given this is newer legislation, how individual states interpret and operationalize changes may vary, so it’s important to check the rules of your state,” said Smitha Walling, head of education savings at Vanguard.

Keep in Mind. The SECURE 2.0 Act says rollovers will adhere to Roth IRA contributions rules and limits, which are set at $7,000 for those under the age of 50 this year. Also, original 529 contributions can be withdrawn tax- and penalty-free, but earnings are subject to taxes and a 10% penalty if they don’t go toward qualified educational expenses, according to the IRS. Some states have their own additional taxes as well.