Good morning.

Now that is a bump.

The stock market has been on a bull run for a little over two years now, but Wall Street’s top executives may be the biggest beneficiaries of all. CEOs in America’s financial industry saw eye-popping pay increases last year, including JPMorgan’s Jamie Dimon, whose comp package climbed more than 8% to $39 million a year. Bank of America’s chief Brian Moynihan took home a 21% raise from 2023, bringing his pay to $35 million. Citigroup’s Jane Fraser took the cake with her salary jumping 33% to $34.5 million. No surprise, Citi shares are up more than 20% this year, and it has been the top performer of the six big banks.

Even with all the inflation, it’s safe to say those raises were more than just cost-of-living adjustments.

Vanguard Took the ETF Asset Crown. Here’s Why It Matters

State Street’s SPDR S&P 500 ETF Trust began its remarkable three-decades long run as the world’s largest exchange-traded fund back in 1993 when The X Files topped Nielsen ratings and MTV’s The Real World was “all that … and a bag of chips.”

Fast forward to today and there’s a new king. Vanguard’s S&P 500 ETF (VOO) finally cemented itself as the undisputed ETF heavyweight topping $632 billion in assets this week, thanks to a record-shattering $116 billion pulled in last year, according to Bloomberg. Now, the Malvern, Pennsylvania company is eyeing BlackRock’s crown as the world’s largest asset manager, and could potentially close the $157 billion gap this year, said Aniket Ullal, head of ETF Research at CFRA. It’s proof that Vanguard’s commitment to low-cost investing is becoming just as popular as Beanie Babies were in the ‘90s.

“Vanguard continues to dominate mindshare,” Ullal told The Advisor Upside. “VOO’s success isn’t just driven by fees, but also by strong brand awareness.”

A-Van Guard

While SPY charges a bargain-basement price of just 0.095% per year to track the S&P 500, VOO’s fee is just 0.03%. Vanguard even doubled down on cost-cutting this month with the largest fee reductions in its 50-year history:

- Equity ETFs now charge roughly five basis points, while fixed income products clock in at just four basis points.

- Almost nine in 10 Vanguard funds are in the lowest-cost decile of their Morningstar categories.

Still, State Street offers a similar S&P 500 fund SPLG that’s priced at 0.02%, less than VOO. Once fees get that low, other factors like brand awareness and distribution become equally important, Ullal said. It’s a strategy Vanguard is taking into new segments. The company launched two active muni-bond ETFs in November with more potentially on the way.

“This is a major milestone for Vanguard and the ETF industry,” said Todd Rosenbluth, head of research at VettaFi.

I, Spy. Hats off to SPY for an unforgettable run. It’s not only the oldest ETF still in existence, but will remain the default fund for the vast majority of institutional investors with its low bid-ask spreads and high trading volumes. With much longer time horizons, clients are simply favoring lower costs. “Much like Babe Ruth, whose records were broken, SPY will remain in the minds of many as a legend,” Rosenbluth said.

Just like Mulder and Scully.

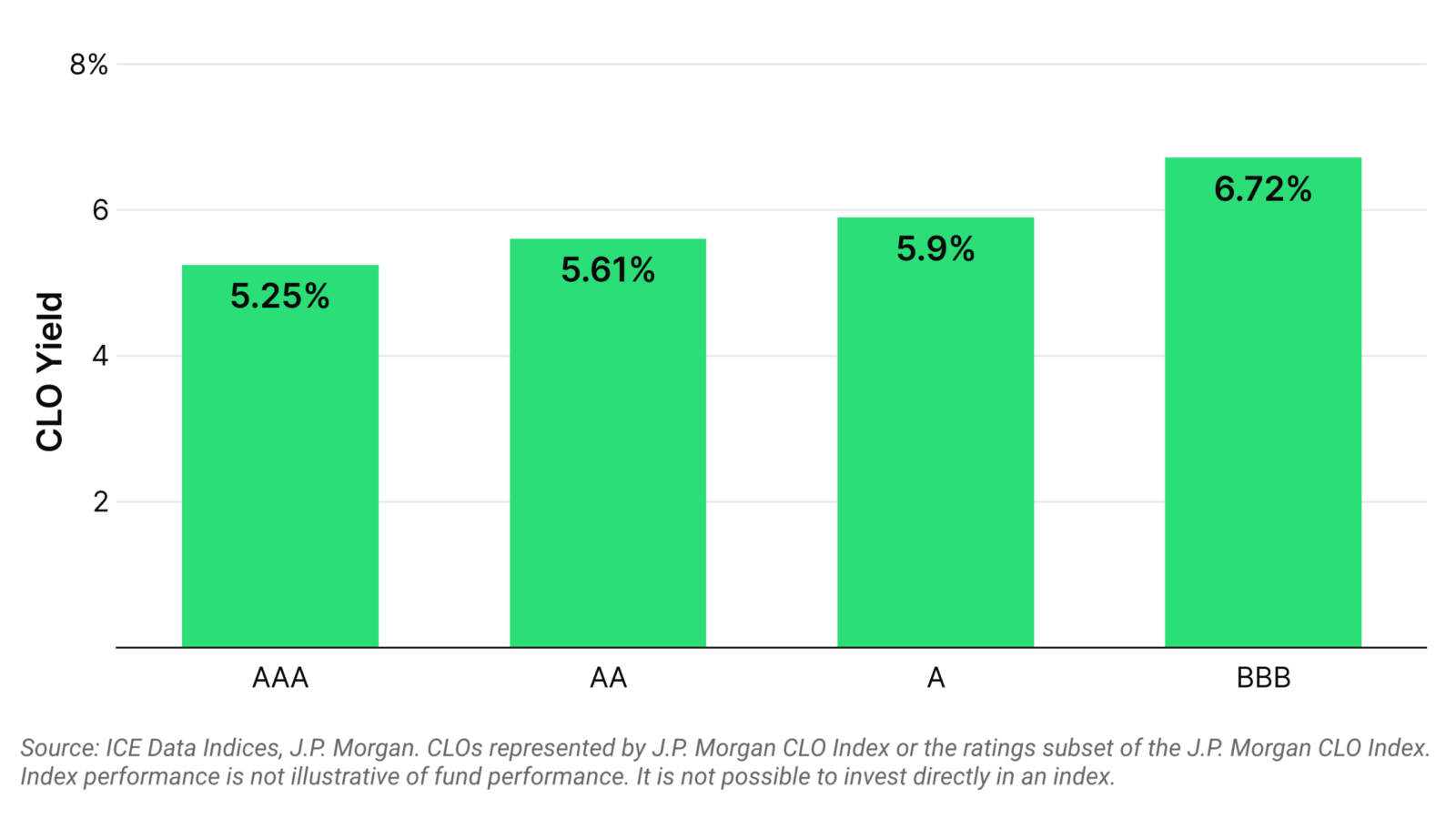

Identifying Value (and Higher Yields) with CLOs

For many advisors, collateralized loan obligations check many of the key boxes when allocating for clients:

- Attractive cash yields — 5.25% within the AAA tranche, and 6.72% for BBB.

- Diversification — the pooled structure protects against single issuer risk, with default rates baked into expected yields.

- Lower Interest Rate Sensitivity — with rates tied to benchmarks such as SOFR and Euribor, CLOs can be a healthy tactic within a diversified strategy.

Advisors newer to the asset class tend to gravitate to AAA-rated CLO tranches due to their perceived safety, but this approach could be leaving returns on the table.

If History Can Tell Us Anything: Over the past decade, Single A CLOs have outperformed AAA CLOs by 142 basis points per year with lower volatility than investment-grade corporate bonds. BBB CLOs, meanwhile, provide a 147 bps yield pickup over AAAs while offering higher credit quality than high-yield bonds.

Active tranche management is key to navigating these nuances and finding relative value within CLOs.

Internet Streamers Need Advice Too. Advisors Are Playing Catch-Up

Smash that “like” button and subscribe.

Like many folks during the pandemic, CPA Ryan Bannister turned to video games for some much-needed human interaction, specifically the live-streaming platform Twitch. What began as a way to talk to others while playing Dark Souls and The Legend of Zelda quickly became “the financial advice hour,” where he informally helped fellow gamers with their finances. In 2022, he launched 1Up Financial Advisors, an RIA that largely targets internet content creators.

“The Mr. Beasts and big streamers of the world are already being taken care of, but I’ve been able to find a sweet spot,” said Bannister, who mostly caters to small- to mid-size creators with six-figure salaries.