Good morning.

The holidays are upon us, and that means it’s time for those 2025 predictions that usually age as well as that carton of eggnog in the back of the fridge.

Has the Fed conquered inflation? Will tariffs weigh on economic growth? Are we living in a gigantic AI bubble? Your guess is as good as ours, but there are a handful of industry trends that will continue to gain steam along the way. What we do know is 2024 was an impressive year for the markets and that generally leads to satisfied customers. Happy clients, happy life.

Let’s dive right in.

(Editor’s note: Due to the holidays and the aforementioned eggnog, we’re taking a break until after the new year. See you Jan. 2.)

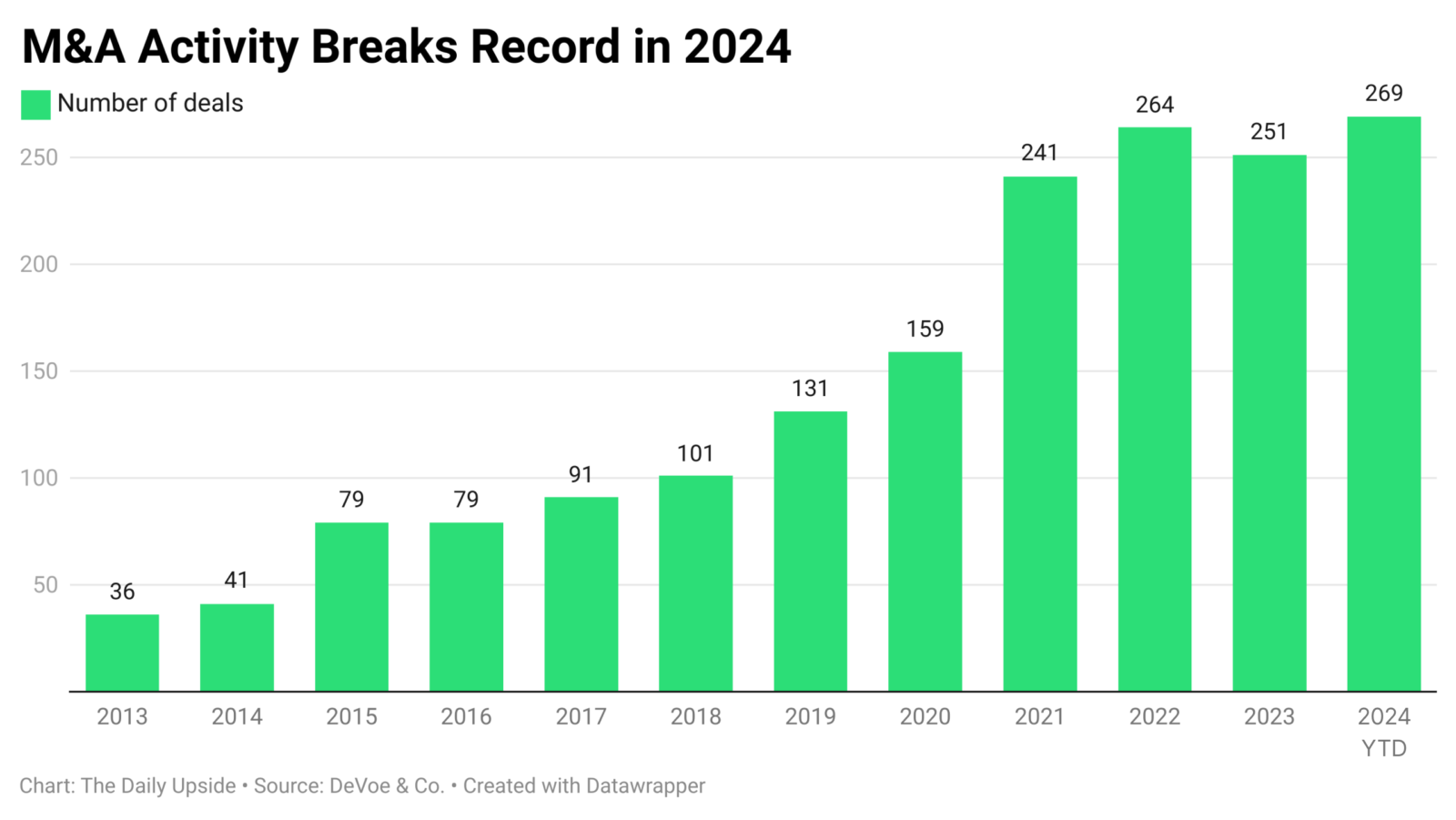

PE Invasion Weighs on Wealth Management

Private equity firms just couldn’t keep their hands off wealth managers in 2024.

With markets roaring and assets hitting all-time highs, there were at least a half a dozen multi-billion-dollar deals that shook the industry this year. Fisher Investments cemented a $3 billion deal in June, followed by Envestnet’s $4.5 billion sale in July, and there were dozens of others. In fact, M&A activity set new records in the registered investment advisor space, with 269 total transactions completed so far in 2024, according to DeVoe & Co. As these massive advisory firms get larger, so do their value propositions. PE investors are expected to become more aggressive in 2025 as interest rates decline, leading to even bigger and more frequent deals, according to the study.

There are certainly questions about how the new powers that be will behave. Some experts question whether PE firms will run into conflicts of interest trying to uphold fiduciary standards, while squeezing out profits for investors. It’s an open ended question that may take years — or, shall we say, fund life cycles — to figure out.

Tip The Scales

PE has been smitten with wealth management for the better part of a decade, and for good reason. By the end of 2029, the value of wealth management firms globally will approach $3 trillion, up from just under $2 trillion last year, according to a report. A Cerulli estimate pegged the opportunity for RIA acquisitions at $3.7 trillion last year. Other major deals this year include:

- TPG’s minority stake in the largest RIA Creative Planning, valuing it at a reported $15 billion.

- CI Financial’s all-cash deal with Mubadala Capital that took it private at a valuation of $8.6 billion.

- PE firm KKR’s purchase of the $150 billion wealth manager Janney Montgomery Scott in July.

- There’s more, but you get the picture.

Not So Fast. What does an influx of PE money mean for the industry as a whole — and for the end clients advisers are trying to serve? Well, all that private equity attention may be starting to take its toll. While private equity brings in more funding, it’s also expecting lucrative profits on tight time tables.

A report from Forrester cited the massive tech provider InvestCloud, which has been majority-owned by Motive Partners and Clearlake Capital since 2021. Earlier this year, the firm raised its service fees 5% despite complaints about slow platform enhancements. If private equity continues to prioritize revenue over platform improvements and customer support, wealth managers may seek alternatives, according to the researchers.

Wall Street’s Hush-Hush Cash Sweeps Take Center Stage

One of Wall Street’s most lucrative, and secretive, revenue streams may be drying up.

The largest broker-dealers have quietly moved clients’ uninvested cash into low-yielding accounts that earned them up to 10 times what they paid out to customers. Called cash sweeps, the programs have been around for decades and one study even found it cost investors upwards of $500 million over a six-year period. Not so much in 2024. Higher yields in everyday saving accounts and a rash of high-profile lawsuits and investigations over the practice are now taking the industry by storm.

It’s forcing clients to rethink their cash strategies and move their assets out of brokerage accounts.

Sweep It Under the Rug

In response, Wells Fargo said in a second-quarter earnings call that it would pay customers more on their cash, and that the firm could take a potential $350 million hit in its wealth arm this year. Not to be outdone, Morgan Stanley quickly announced it would pay its clients 2% in July. The company also announced a revenue loss in its sweep accounts, which topped $1.798 billion for the second quarter, down 17% from a year ago. Some dozen firms are now facing legal challenges:

- Customers alleged Morgan Stanley broke its fiduciary duty to clients by paying just 0.01% on uninvested cash, far below market rates.

- JPM faced a similar class-action lawsuit over the bank channeling customers’ idle cash into low interest rate accounts.

- Raymond James also got caught up in the lawsuit maelstrom this time alleging it only paid customers 0.25% to 3%, significantly lower than average.

The sweep programs, known in earnings reports as Net Interest Income, weren’t all cash grabs though. The additional revenue often subsidized other parts of the business. For example, it allowed low-cost pioneers, like Charles Schwab (who was the first to pay an SEC penalty over the matter in 2022), to offer their robo advisors for free, but forced them to keep a percentage of their assets in cash.

Dollar Here, Dollar There. The firms are looking for ways to supplement the lost revenue. Charles Schwab executives said the firm will look toward expanding its advice offering to retail clients in the new year, especially those that are being ported over in the TD Ameritrade deal. Those financial advice relationships are a lucrative and predictable fee-based revenue stream.

Addressing losses to its NII accounts, Morgan Stanley’s CFO Sharon Yeshaya said it was due to changes in the competitive dynamics. They’re expected to be offset by “repricing” the overall investment portfolio, she said.