The Not-So-Transparent Fees Hiding in the ETF Market

Not required to be disclosed, index licensing fees create a thin layer of fog over the transparent investment products.

Sign up for exclusive news and analysis of the rapidly evolving ETF landscape.

Exchange-traded funds are known for being pretty transparent, but there’s one cost that’s largely undisclosed.

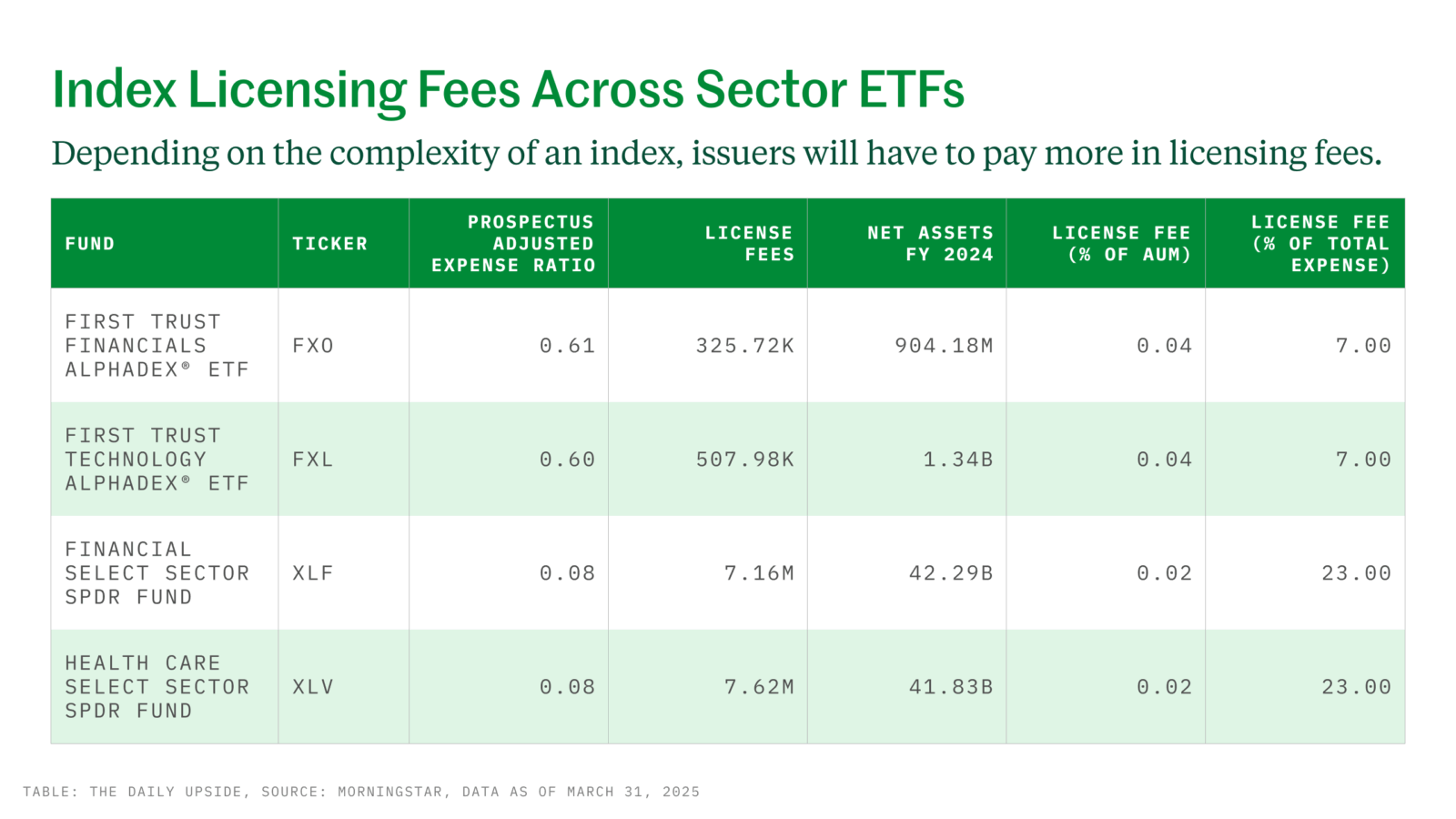

Licensing fees are paid by issuers to the index provider for the right to use their benchmarks, and they can make up more than a quarter of the total expense ratio of the products, according to a Morningstar analysis. The fees aren’t required to be disclosed, but even when asset managers do include them, the costs can be difficult to find, said Lan Anh Tran, manager research analyst for Morningstar. While the fees are generally small, they create a layer of fog over the otherwise transparently priced products.

“It’s not something that we’re happy about,” Tran told ETF Upside.

How Do License Fees Work?

Licensing fees vary depending on the index a fund tracks, with some funds paying more for more complex indexes. For example, as a percentage of assets, First Trust’s AlphaDEX ETFs pay roughly double the licensing fees of State Street’s SPDR funds, Morningstar highlighted. That’s because AlphaDEX tracks ICE Data Indices designed to outperform sectors through growth and value factors, while SPDR ETFs simply mimic traditional S&P sector indexes. However, because the First Trust ETFs have higher expense ratios, their licensing fees make up only 7% of total cost to investors, compared with about 25% for the SPDR funds.

How Low Can You Go? Tran noted that many new ETFs aim for niche or strategic beta exposures, rather than tracking traditional indexes. “With the complexity that comes with those strategies, I doubt there’s going to be a trend toward cheaper costs for index providers,” she said.

One way some issuers have reduced costs, though, is by switching indexes. Morningstar highlighted Vanguard’s 2013 move from MSCI to CRSP indexes, which lowered expense ratios by 1–2 basis points per fund. But switching isn’t easy. “Changing an index is a very complicated, costly, and disruptive process,” Tran said, adding that a lower licensing fee is often a benefit — but not the primary motivation. “Asset managers aren’t just looking for the cheapest option, jumping from index to index,” she said.

Recent News

-

Capital Group, Dimensional Top Active ETF Inflows Amid Volatility

Photo via Connor Lin / The Daily Upside

-

Allspring’s Latest Clones Are Active Growth, Value ETFs

Photo via Connor Lin / The Daily Upside